White Economic Advantage + Black Economic Suppression

=

Modern Vectors of Economic Oppression

"That racial bias was built into these (burial) policies was long an open secret in the insurance industry. Insurance forms asked the applicant’s race, and blacks were routinely charged more than whites for the same coverage, the insurance industry now publicly acknowledges." Typically, it was one third more, according to lawyers representing black policy holders.

Joanne Stone Morrissey, president of the insurance researcher Firemark Group in Morristown, N.J.

Overview

Summary

Insurance has been a central—but often invisible—driver of the racial wealth gap, beginning with slavery-era policies that treated Black life as commercial property and continuing through 20th-century redlining, race-based premiums, and the extraction of wealth through predatory burial and industrial life policies. Even after civil rights reforms, insurers replaced explicit racial discrimination with actuarial proxies such as ZIP code, credit score, education, and property valuation—variables that encode the legacy of segregation, policing disparities, and economic exclusion. These practices inflate premiums for Black families, depress claim payouts, and leave Black homes, cars, businesses, and health more exposed to risk. Today, algorithmic underwriting, climate-driven non-renewals, and unequal disaster recovery widen these inequities, while centuries of underinsurance and lower compensation reduce the ability to build, protect, and transfer wealth across generations. When aggregated, insurance discrimination accounts for an estimated 8–12% of the racial wealth gap, making it one of the most under-recognized vectors of modern economic oppression.

Personal Narratives

“Even though plantation slaves were valuable in the marketplace, they were never insured,” Ralph said. “They were viewed more as livestock. They enhanced the value of the plantation but their skills weren’t seen as valuable or premium.” Instead, slave owners would insure coal miners, Blacksmiths, carpenters, railroad workers and other slaves with valued skills. Miners, for example, made up 15.4 percent of the insured slave workforce, according to the project. Steamboat workers accounted for 12.6 percent of those insured and domestic workers accounted for 14.6 percent of the insured slave population, according to the ledger.”

New York University Professor Michael Ralph

Visualizing the slave insurance industry.

*****************

In 2005, JP Morgan Chase conceded that two of its subsidiaries Citizens' Bank and Canal Bank in Louisiana accepted enslaved people as collateral for loans.

Historical analysis conducted for J.P. Morgan by History Associates Inc. of Rockville found that between 1831 and 1865 the two banks accepted approximately 13,000 slaves as collateral and ended up owning about 1,250 slaves.

Timelines of Disparity

Enslavement and Antebellum Era (Pre-1865)

Mechanisms of Oppression

Insurance companies in the United States and Europe developed products that treated enslaved people as insurable property. Life insurance policies compensated enslavers for the death of enslaved laborers. Marine insurers underwrote slave ships, covering enslaved individuals as “cargo,” and plantation owners insured crops, structures, and enslaved labor as part of their commercial operations. These policies stabilized the financial infrastructure of slavery and tied the insurance industry’s early profits directly to the commodification of Black life.

Accumulating Effects

The foundational practices of insuring enslaved people normalized viewing Black life as a financial asset for white wealth accumulation. Insurance firms grew rich from slavery-linked premiums and payouts, capital that later funded corporate expansion. Black families, by contrast, began post-emancipation with no access to life insurance, burial insurance, or property coverage—placing them on unequal footing in the emerging financial economy.

Sources

Acknowledging our past: New York Life and slavery

Our historical links to the transatlantic slave trade - Lloyd's

Visualizing the slave insurance industry | TechCrunch

Reconstruction and Retrenchment (1865–1915)

Mechanisms of Oppression

As formerly enslaved people sought economic independence, insurance companies refused to sell policies to Black people or offered only exploitative “industrial life” policies with high premiums and low benefits. Insurers used race-based actuarial tables to justify charging Black customers more. Meanwhile, white wealth accumulated through insured farms, businesses, and homes, while Black landholders—often using heirs’ property—faced exclusions, refusals of coverage, and discriminatory claims settlement.

Accumulating Effects

Black families attempting to build wealth were structurally prevented from obtaining protective or generative insurance products (life, fire, property, business). Low-value industrial policies extracted wealth while offering almost no long-term accumulation or security. These disparities widened the early post-slavery racial wealth gap.

Sources

1800s | Black History and the Evolution of the Insurance Industry in America

State Health Equity Initiatives and Racism in Insurance Industry | Commonwealth Fund

Redlining, Segregation, and Actuarial Codification (1915–1968)

Mechanisms of Oppression

Insurance companies systematically aligned their underwriting practices with emerging segregationist norms. Homeowners’ insurance was denied in Black neighborhoods through redlining maps, and auto insurance premiums were tied to racially segregated ZIP codes. Race-based life insurance premiums remained common. Industrial life policies continued extracting wealth from Black communities. Insurers embedded neighborhood racial composition, credit barriers, and policing data into actuarial models—locking racial bias into industry standards.

Accumulating Effects

The denial of fair home insurance reinforced housing segregation, limiting access to mortgages and suppressing Black home equity. Racialized auto insurance pricing increased the cost of mobility and work. Families unable to obtain fair life or property coverage were locked out of generational wealth protection mechanisms while white families’ insured assets appreciated.

Sources

Calculating Race: Racial Discrimination in Risk Assessment - Actuary.org

Civil Rights to Deregulation (1968–2000)

Mechanisms of Oppression

Although explicit racial discrimination became illegal after the Fair Housing Act, insurers replaced race with proxies: credit scores, ZIP codes, home age, occupation, and education levels. These variables tracked closely with racial segregation and economic exclusion. Insurers increasingly used computer-based actuarial models that absorbed racially biased data. Disparate claims payouts, higher premiums, and continued denials persisted, especially in predominantly Black neighborhoods.

Accumulating Effects

The shift from explicit discrimination to data-driven proxy discrimination cemented racial inequities in insurance access and cost. Wealth and property values in Black neighborhoods stagnated or declined due to underinsurance, lower claims payouts, and predatory insurance-linked loan products. The private insurance industry became a major, though often invisible, engine of racial wealth stratification.

Sources

Algorithmic Discrimination, Climate Risk, and Disaster Recovery (2000–2020)

Mechanisms of Oppression

Machine-learning underwriting systems intensified disparities by relying on biased data sets reflecting segregation, credit discrimination, and policing. Climate-related non-renewals disproportionately targeted Black neighborhoods located in environmentally hazardous areas shaped by historic racism. After natural disasters, insurers more often delayed or denied claims from Black homeowners and undervalued property in Black neighborhoods. Forced-placed insurance and premium financing schemes targeted Black borrowers at higher rates.

Accumulating Effects

As climate change accelerated, Black homeowners—already more likely to live in at-risk areas and have undervalued homes—faced spiraling premiums or policy cancellations. Post-disaster recovery gaps widened the racial wealth divide as white households rebuilt quickly while Black households suffered uncompensated losses. Algorithmic underwriting scaled inequity nationally.

Sources

Contemporary Era of Racialized Risk (2020–Present)

Mechanisms of Oppression

Insurers continue using race-correlated variables such as ZIP code, credit score, and education to set premiums. Disparities in property valuation produce underinsurance in Black communities. Auto insurance remains more expensive for Black drivers even with identical driving histories. Post-disaster claims disparities persist, and climate-driven withdrawals from “high-risk” markets disproportionately harm Black neighborhoods. Insurers have not corrected the historical accumulation of wealth derived from slavery-linked practices.

Accumulating Effects

Insurance discrimination today reduces Black households’ ability to protect wealth, recover from disasters, invest in property, and pass down intergenerational assets. These disparities amplify the racial wealth gap by increasing costs, reducing payouts, and imposing disproportionate risk exposure—creating a system in which Black families pay more for less protection.

Sources

Why Stopping Algorithmic Inequality Requires Taking Race Into Account – The Markup

Metrics: How Insurance Oppression Contributes to the Racial Wealth Gap

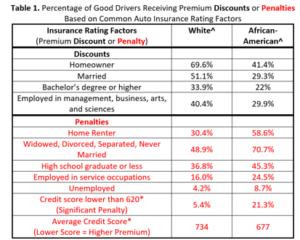

“African-Americans are disproportionately represented in the higher premium categories, as Table 1 illustrates, which leads to higher prices for the exact same coverage, even before considering geographic pricing disparities. CFA found, in a 2015 report, that ZIP codes with predominantly African American residents face premiums that are 60% higher than predominantly white ZIP codes, after adjusting for population density. Taken all together, it is clear that African Americans will pay more for auto insurance than white drivers, even when everything related to driving safety and vehicle type is held constant.” [5]

Methods of Discrimination

Actuarial Bias in Risk Modeling

Racial bias becomes embedded in actuarial formulas when they rely on historical datasets shaped by segregation, policing disparities, environmental racism, and redlining. These algorithms treat race-correlated variables—ZIP code, credit score, claims history—as “objective,” producing discriminatory premiums and coverage decisions. Because actuarial models drive nearly every form of insurance, biased inputs create a system-wide transfer of wealth away from Black families.

Beginning in the early 20th century, many companies charged Black policyholders more for less coverage using race-based actuarial tables. Some companies maintained separate Black and white actuarial structures deep into the 20th century, and lawsuits continue into the present.

Sources:

Calculating Race: Racial Discrimination in Risk Assessment - Actuary.org

Race & Insurance

Algorithms in Underwriting Discrimination

Insurers increasingly rely on machine-learning systems that use proxies like location, education, credit profile, and past claims. Because these features correlate strongly with racial segregation and economic exclusion, automated underwriting reproduces discriminatory outcomes at scale while masking bias under a veneer of technological neutrality.

Sources:

Why Stopping Algorithmic Inequality Requires Taking Race Into Account – The Markup

Asset-Based Pricing Penalties

Insurance products often reward accumulated wealth (homeownership, assets, financial history) with lower premiums, while charging more to households without these assets. Because racialized policies created massive wealth gaps, asset-linked insurance pricing punishes Black households for structural deprivation they did not cause, deepening disparities in financial stability and intergenerational wealth transmission.

Sources:

Auto Insurance Rate Disparities Based on ZIP Code

Black drivers pay hundreds more per year for car insurance even when factors like driving record, vehicle, and background risk are the same. Insurers justify these disparities using territorial rating systems rooted in redlining-era maps and policing patterns that inflate risk scores in Black neighborhoods.

Sources:

- DC Department of Insurance, Securities and Banking Reveals Findings of Study on Potential Racial Bias in Auto Insurance Premiums |

- How We Examined Racial Discrimination in Auto Insurance Prices — ProPublica

- Bills take aim at zip code-based auto insurance rates

- Regulators move to study racism in insurance industries. Experts say it's not enough.

- The Color of Property and Auto Insurance: Time for Change

Banking & Credit-Linked Insurance Denials

Many insurance products require or are linked to banking products—mortgages, auto loans, small-business loans, home equity. Because Black borrowers face discriminatory interest rates, credit scoring, and denial rates, they are more likely to be steered into subprime or higher-risk insurance markets or denied insurance entirely.

Burial & Life Insurance “Industrial Policies” Targeting Black Families

From the late 19th to mid-20th century, insurers sold “industrial life” policies door-to-door in Black neighborhoods—charging high premiums for tiny death benefits. These exploitative products extracted wealth from Black families while offering virtually no long-term value, forming a critical bridge between slavery-era exploitation and modern insurance discrimination.

Sources:

MetLife Is Settling Bias Lawsuit - The New York Times

• https://scholarlycommons.law.northwestern.edu/cgi/viewcontent.cgi?article=1041&context=njlsp

Climate-Risk-Based Non-Renewals Disproportionately Affecting Black Homeowners

Insurers increasingly refuse coverage in areas labeled as “high climate risk”—often the same neighborhoods subjected to decades of environmental racism, industrial zoning, and disinvestment. This exposes Black homeowners to catastrophic uninsured loss.

Sources:

The Climate Insurance Crisis Is Crushing Black Homeownership - America's Black Holocaust Museum

Credit Score-Based Discrimination

Credit-based insurance scores lead Black consumers to pay higher rates even when claims histories and driving records are equivalent. Because credit scores themselves are racially biased artifacts of employment discrimination, redlining, and credit access disparities, this pricing system is structurally inequitable.

Disparate Claims Payouts for Property Damage

Studies show that insurers pay lower amounts for similar claims in Black neighborhoods. Surveyors may undervalue property, offer smaller settlements, or delay payouts—reducing recovery after disasters and eroding home equity.

Hurricanes, floods, and fires lead to significantly slower and lower payouts in predominantly Black neighborhoods. These discrepancies compound vulnerability after disasters, deepening the racial wealth gap through unequal recovery.

Floods, mold, industrial contamination, and lead exposure are more common in Black neighborhoods due to environmental racism. Insurers classify these as “uninsurable hazards,” denying coverage or charging exorbitant premiums, which leaves Black property owners disproportionately exposed.

Sources:

Race Discrimination in the Adjudication of Claims: Evidence from Earthquake Insurance

Biased Fraud Detection & Claims Investigation

Black claimants are more likely to have their claims flagged for fraud or subjected to invasive investigation. These disparities stem from biased algorithms, stereotypes about criminality, and structural policing patterns that insurers treat as objective risk data.

Sources:

• Where State Farm Sees ‘a Lot of Fraud,’ Black Customers See Discrimination - The New York Times

Benefit Denial for Pre-Existing Conditions Linked to Structural Inequity

Black Americans experience higher rates of chronic conditions due to medical racism, toxic exposure, food apartheid, and environmental harms. Insurers historically penalized these conditions by denying coverage or charging higher rates—even though the conditions stemmed from structural inequity rather than personal behavior—exacerbating health and wealth gaps.

Sources:

Structural Racism In Historical And Modern US Health Care Policy | Health Affairs

Health Insurance Coverage Gaps Linked to Discrimination

Occupational segregation and discriminatory hiring reduce access to employer-sponsored health insurance for Black workers. This creates higher out-of-pocket costs and worse health outcomes that cascade into lost income and reduced wealth.

Exclusions for Heirs’ Property Owners

Families who inherited land informally without a will (heirs’ property)—often due to discriminatory legal structures—are unable to obtain insurance because insurers require clear title. This leaves homes unprotected from disaster and accelerates Black land loss.

Discriminatory Rate Setting in Home Insurance

Insurers charge higher rates in Black neighborhoods using factors such as perceived crime, aging housing stock, or “market volatility”—all rooted in historical redlining and municipal disinvestment. Even when controlling for risk, premiums remain significantly higher.

Insurance companies often provide discounts and better coverage for homeowners than renters—yet Black families are disproportionately renters due to racist housing policy. This creates a structural penalty on those excluded from homeownership.

The Fair Housing Act and Disparate Impact in Homeowners

Insurance

Redlining in Property, Auto, and Life Insurance

Insurance redlining—denying coverage or charging inflated premiums in Black neighborhoods—is one of the central historical mechanisms linking insurance to the racial wealth gap. Even long after redlining was outlawed, underwriting maps, zoning classifications, and claims histories continue to mirror racially segregated geographies.

Sources:

Calculating Race: Racial Discrimination in Risk Assessment - Actuary.org

The Color of Property and Auto Insurance: Time for Change

Slavery-Era Life Insurance Policies on Enslaved People

From the 1830s through the Civil War, insurance companies sold policies that insured enslavers against the death of enslaved laborers. These policies treated enslaved people as insurable property, enriching financial institutions while cementing the commodification of Black life as a foundation of modern insurance practices.

Sources:

Slave-Era Insurance Policies and Their Impact | BPOG

____________________________________________________

New York Life, the nation’s third-largest life insurance company, opened in Manhattan’s financial district in the spring of 1845. The firm possessed a prime address — 58 Wall Street — and a board of trustees populated by some of the city’s wealthiest merchants, bankers and railroad magnates.

Sales were sluggish that year. So the company looked south.

There, in Richmond, Va., an enterprising New York Life agent sold more than 30 policies in a single day in February 1846. Soon, advertisements began appearing in newspapers from Wilmington, N.C., to Louisville as the New York-based company encouraged Southerners to buy insurance to protect their most precious commodity: their slaves.

Alive, slaves were among a white man’s most prized assets. Dead, they were considered virtually worthless. Life insurance changed that calculus, allowing slave owners to recoup three-quarters of a slave’s value in the event of an untimely death.

James De Peyster Ogden, New York Life’s first president, would later describe the American system of human bondage as “evil.” But by 1847, insurance policies on slaves accounted for a third of the policies in a firm that would become one of the nation’s Fortune 100 companies."

Rachel L. Swarns

Sources:

Insurance Policies on Slaves: New York Life’s Complicated Past - The New York Times (nytimes.com)

Acknowledging our past: New York Life and slavery

________________________________________________________________

In 2005, JP Morgan Chase conceded that two of its subsidiaries Citizens' Bank and Canal Bank in Louisiana accepted enslaved people as collateral for loans.

Historical analysis conducted for J.P. Morgan by History Associates Inc. of Rockville found that between 1831 and 1865 the two banks accepted approximately 13,000 slaves as collateral and ended up owning about 1,250 slaves.

Sources:

Our historical links to the transatlantic slave trade - Lloyd's

Visualizing the slave insurance industry | TechCrunch

____________________________________________________

On September 30, 2000, Governor Gray Davis of California signed two bills relating to slave insurance. One bill was written by former California State Senator Tom Hayden. The California legislature found that:

Insurance policies from the slavery era have been discovered in the archives of several insurance companies, documenting insurance coverage for slaveholders for damage to or death of their slaves, issued by a predecessor insurance firm. These documents provide the first evidence of ill-gotten profits from slavery, which profits in part capitalized insurers whose successors remain in existence today.

Sources:

Slavery Era Insurance Registry Report

Slave insurance in the United States - Wikipedia

1800s | Black History and the Evolution of the Insurance Industry in America

State Health Equity Initiatives and Racism in Insurance Industry | Commonwealth Fund

Slavery-Era Maritime & Transport Insurance on Slave Ships

Marine insurers—including Lloyd’s—covered slave ships, cargo, and enslaved people as commercial property, creating a direct financial incentive for the continuation of the transatlantic slave trade. Some insurers reimbursed slavers for the deaths of enslaved people lost at sea.

Sources:

Our historical links to the transatlantic slave trade - Lloyd's

African American Maritime History Series #2: Emergent Marine Insurance and Insuring the Enslaved

Slavery-Era Plantation Insurance

Insurance companies protected enslaved plantations against losses due to fire, crop failure, and property damage—stabilizing the financial viability of the slave economy. These policies helped enslavers accumulate wealth that carried forward into institutional and family fortunes today.

Sources: